CryptoChain Blog

CryptoChain Blog

Introduction to 2026 CBDC Developments

Central bank digital currencies (CBDCs) are rapidly advancing in 2026, fundamentally altering how payments flow across borders. Unlike decentralized cryptocurrencies such as Bitcoin, CBDCs are issued and regulated by central banks, offering a digital form of sovereign money. Governments worldwide are accelerating these projects to modernize payment infrastructure, enhance financial inclusion, and compete in the evolving digital economy. This comprehensive guide examines the latest implementations, real-world pilot programs, and their broader implications for users and businesses seeking timely cryptocurrency news and adoption insights.

Readers interested in blockchain updates will find detailed coverage of how these state-backed digital currencies integrate with existing financial systems while addressing challenges like scalability and cross-border compatibility.

Key CBDC Launches in Asia, Europe, and the Americas

In Asia, China's e-CNY has expanded significantly, with ongoing trials involving high-volume retail transactions and cross-border settlements with neighboring economies. India's digital rupee pilot has grown to encompass multiple states, focusing on both wholesale and retail applications that support small merchants and everyday consumers. Singapore and South Korea are also advancing their respective projects, emphasizing interoperability with regional payment networks.

Europe’s digital euro initiative has entered advanced testing phases, with several commercial banks participating in simulations for wholesale settlements and programmable money features. The European Central Bank continues to refine design choices around offline capabilities and privacy protections.

In the Americas, Brazil’s Drex platform has progressed through multiple pilot stages, demonstrating use cases in interbank transfers and tokenized asset settlements. The Bahamas Sand Dollar remains a leading example of a fully operational CBDC, serving as a model for smaller island nations. Meanwhile, the United States Federal Reserve is conducting exploratory research on a potential digital dollar, evaluating impacts on monetary policy and payment efficiency. These case studies highlight diverse approaches tailored to local economic needs and technological readiness.

CBDCs vs Decentralized Cryptocurrencies: A Detailed Comparison

Understanding the distinctions between CBDCs and decentralized cryptocurrencies is essential for anyone navigating 2026 crypto news. CBDCs provide centralized control, ensuring price stability pegged directly to national fiat currencies, whereas decentralized options like Ethereum or stablecoins often experience market-driven fluctuations.

- Control and Stability: Central banks manage supply and monetary policy for CBDCs, reducing volatility risks that affect cryptocurrencies. This makes CBDCs more suitable for everyday payments and savings.

- Privacy Features: CBDC architectures typically incorporate tiered privacy, allowing limited anonymity for small transactions while enabling traceability for larger ones to comply with regulations. In contrast, many decentralized cryptocurrencies prioritize pseudonymity or full anonymity through advanced cryptography.

- Adoption Barriers: Regulatory support accelerates CBDC rollout but introduces concerns about government oversight. Decentralized cryptocurrencies offer greater user autonomy yet face hurdles like exchange volatility and limited merchant acceptance in some regions.

- Transaction Speed and Cost: CBDCs leverage existing central bank infrastructure for near-instant settlements at minimal or zero fees in domestic use, while decentralized networks may incur variable gas fees depending on congestion.

Many analysts view CBDCs as complementary tools that could coexist with decentralized assets, enabling hybrid financial ecosystems.

Regulatory Hurdles and Integration Challenges

Implementing CBDCs involves overcoming significant regulatory and technical barriers. Data protection laws, such as those modeled on global standards, require careful balancing of transparency for anti-money laundering purposes with user privacy rights. Integration with legacy payment rails demands close coordination between central banks, commercial institutions, and technology providers to ensure seamless interoperability.

Cross-border challenges include differing legal frameworks and currency conversion mechanisms. The Bank for International Settlements provides ongoing research and frameworks on these topics at https://www.bis.org/. Additional insights from international organizations like the International Monetary Fund are available at https://www.imf.org/. Policymakers must also address cybersecurity risks and establish clear liability rules for digital currency losses or disputes.

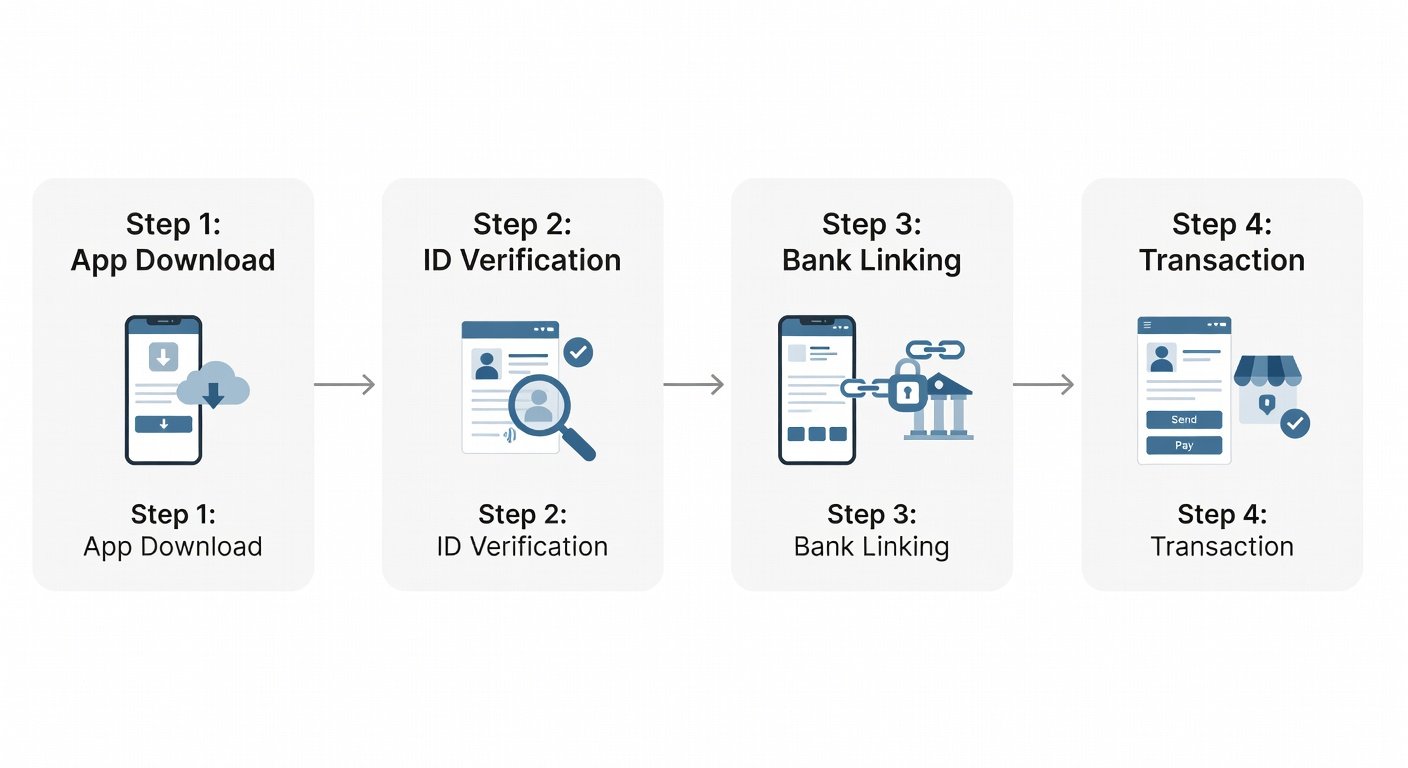

Step-by-Step User Onboarding for CBDC Wallets

Practical adoption begins with straightforward wallet setup processes designed for broad accessibility. Here is a detailed overview of typical onboarding steps observed in active 2026 pilots:

- Download an official central bank-approved wallet application from authorized app stores or government portals to avoid counterfeit versions.

- Complete identity verification by uploading government-issued identification documents and performing biometric authentication such as facial recognition or fingerprint scans.

- Link an existing traditional bank account for seamless funding or visit authorized agent locations to deposit physical cash directly into the digital wallet.

- Configure advanced security settings, including multi-factor authentication, transaction limits, and recovery phrases for account restoration.

- Verify the wallet through a test transaction or confirmation code sent via SMS or email before initiating real payments with merchants or peers.

- Explore additional features such as bill payments, peer-to-peer transfers, and integration with merchant point-of-sale systems once the account is active.

This structured approach minimizes friction and supports users with varying levels of digital literacy, often completing the entire process in under 20 minutes.

Impacts on Remittances and Cross-Border Payments

CBDCs are poised to transform international remittances by reducing processing times from days to seconds and lowering associated costs through direct central bank channels. In regions with high migrant worker populations, such as parts of Latin America and Southeast Asia, early pilots have shown improved access for recipients without traditional bank accounts.

Examples include enhanced corridors between Asian economies where digital currency settlements bypass multiple intermediary banks. The World Bank continues to track these developments and their effects on global financial flows at https://www.worldbank.org/. Businesses involved in e-commerce also benefit from faster settlement cycles and reduced currency conversion friction when operating across CBDC-enabled jurisdictions.

Privacy and Accessibility: Addressing Common Concerns

FAQ Section:

Q: How private are CBDC transactions? A: Most designs incorporate privacy tiers, balancing user anonymity for routine payments with necessary oversight for regulatory compliance and fraud prevention.

Q: Will CBDCs be accessible in rural or low-connectivity areas? A: Yes, many programs incorporate offline transaction capabilities and extensive agent networks to serve populations without reliable internet access.

Q: Can I use CBDCs alongside cryptocurrencies? A: Integration is possible through hybrid wallet solutions in several jurisdictions, allowing users to hold and exchange both forms of digital assets.

Q: What happens if I lose access to my CBDC wallet? A: Recovery mechanisms typically involve verified identity processes with the issuing central bank or authorized financial institutions to restore funds securely.

Q: Are there age or eligibility restrictions for CBDC use? A: Eligibility generally aligns with existing banking regulations, often requiring users to meet minimum age and residency requirements similar to traditional accounts.

Conclusion

As 2026 progresses, CBDC rollouts continue to reshape global finance by offering efficient, regulated alternatives to traditional payment methods. Individuals and businesses that understand these developments can better position themselves for the future of money. Ongoing monitoring of pilot results and policy updates remains essential for informed decision-making in the cryptocurrency and payments space.

No comments yet. Be the first!