CryptoChain Blog

CryptoChain Blog

Introduction to CBDCs and Cryptocurrencies in 2026

In 2026, the financial world is witnessing a seismic shift as Central Bank Digital Currencies (CBDCs) gain traction alongside traditional cryptocurrencies like Bitcoin and Ethereum. CBDCs are digital versions of fiat money issued by central banks, while cryptocurrencies operate on decentralized blockchains. This comparison explores adoption rates, technological differences, regulatory influences, competitive dynamics, and their effects on trends like DeFi and payments. Investors navigating this landscape need actionable insights to position themselves effectively.

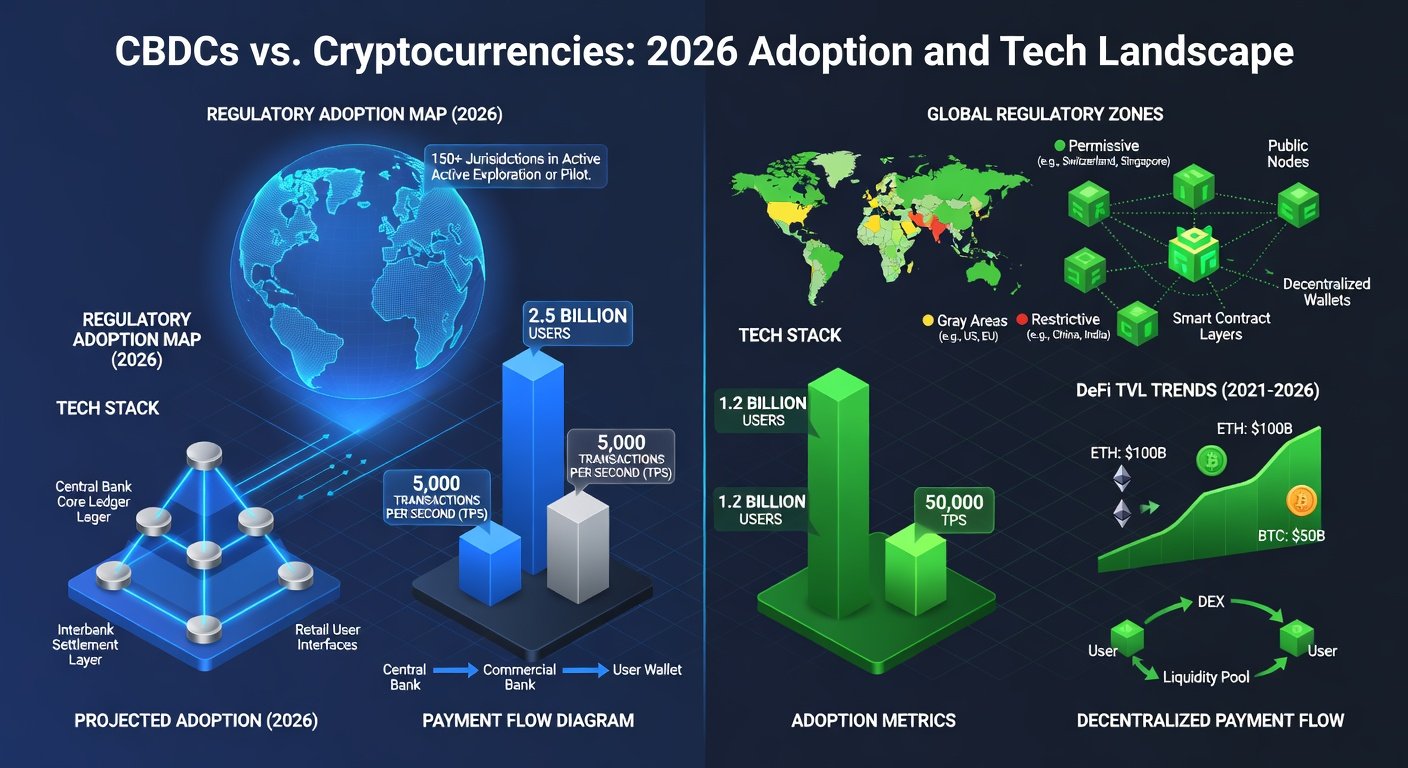

By mid-2026, over 130 countries are piloting or launching CBDCs, per reports from global institutions. Meanwhile, crypto market cap hovers around $3 trillion, driven by institutional adoption. Understanding these forces is crucial for spotting opportunities and risks.

Adoption Rates: CBDCs Closing the Gap

CBDC adoption has accelerated dramatically. China's e-CNY boasts over 300 million users, integrated into daily payments via apps like WeChat. The European Central Bank's digital euro is in advanced trials, targeting a 2026 launch for cross-border efficiency. In the US, the Federal Reserve's digital dollar pilots are expanding, focusing on financial inclusion.

Contrast this with cryptocurrencies: Bitcoin's user base exceeds 500 million wallets, but active daily users lag behind traditional finance. Ethereum powers DeFi with $100B+ in locked value. Adoption metrics show CBDCs leading in retail use—e.g., Bahamas' Sand Dollar at 40% national penetration—while crypto dominates speculative and borderless transfers.

- CBDC Strengths: Government-backed trust, seamless integration with existing banking.

- Crypto Strengths: Global accessibility, pseudonymity.

By 2026, hybrid models emerge, with 20% of global payments potentially CBDC-driven, per IMF estimates, pressuring crypto's retail share.

Technological Differences: Centralized vs Decentralized

CBDCs typically use permissioned ledgers or centralized databases, prioritizing scalability and privacy controls. For instance, many employ Distributed Ledger Technology (DLT) like Hyperledger but without public consensus mechanisms. This allows transaction speeds of millions per second, far surpassing Bitcoin's 7 TPS or Ethereum's 30 TPS (pre-sharding upgrades).

Cryptocurrencies rely on public blockchains with proof-of-work (PoW) or proof-of-stake (PoS). Ethereum's 2022 Merge to PoS improved efficiency, but CBDCs avoid energy-intensive mining. Smart contracts are crypto's edge, enabling DeFi protocols absent in most CBDCs.

| Aspect | CBDC | Cryptocurrency |

|---|---|---|

| Consensus | Centralized/ Permissioned | Decentralized (PoW/PoS) |

| Scalability | High (10k+ TPS) | Variable (Layer 2 solutions) |

| Privacy | Regulated anonymity | Pseudonymous |

Tech convergence is evident: Some CBDCs integrate blockchain interoperability, blurring lines.

Regulatory Influences Shaping the Landscape

Regulations heavily favor CBDCs. Central banks set rules ensuring stability, like the Bank for International Settlements (BIS) guidelines on interoperability. The EU's MiCA framework bolsters euro CBDC while scrutinizing stablecoins.

Cryptocurrencies face fragmented regs: US SEC crackdowns on unregistered securities contrast with El Salvador's Bitcoin legal tender. By 2026, G20 harmonization efforts reduce crypto's regulatory arbitrage but stifle innovation. This tilts competition toward CBDCs for institutional use.

Competitive Dynamics: Who Wins?

CBDCs compete directly in payments, eroding crypto's remittance dominance (e.g., Stellar or Ripple). However, crypto's composability fuels DeFi, with protocols like Aave and Uniswap processing $1T+ annually. CBDCs may interoperate via bridges, creating hybrid ecosystems.

Market share projections: CBDCs capture 15-25% of cross-border payments by 2030, per IMF data, pressuring altcoins. Yet, Bitcoin remains a store-of-value hedge against fiat debasement.

Effects on DeFi and Payments Trends

DeFi TVL could dip 10-20% if CBDCs offer yield-bearing accounts with lower risk, drawing liquidity from high-APY farms. However, CBDC programmability (e.g., expiring stimulus) might boost DeFi innovation, like wrapped CBDC tokens on Ethereum.

In payments, Lightning Network and Solana challenge Visa, but CBDCs integrate natively with merchants. Expect DeFi to pivot toward niche privacy (Zcash) and yield optimization.

- Opportunities: CBDC-DeFi bridges for tokenized assets.

- Risks: Regulatory silos fragment liquidity.

Actionable Market Insights for Investors

1. **Diversify into Interoperable Chains:** Bet on Polkadot or Cosmos for CBDC bridges. Allocate 20% portfolio.

2. **Stablecoin Plays:** USDC/Tether face pressure; favor algorithmics or CBDC-pegged variants.

3. **Layer 2 Scaling:** Arbitrum/Optimism for DeFi resilience amid CBDC scalability.

4. **Monitor Pilots:** Track Federal Reserve updates; US digital dollar success boosts legacy banks' crypto arms (e.g., JPM Coin).

5. **Hedge with BTC/ETH:** Core holdings for volatility; target 40% allocation.

Risk management: Set 10% stops on altcoins; watch BIS reports for policy shifts. In 2026, winners blend fiat stability with crypto innovation.

Conclusion

CBDCs and cryptocurrencies aren't zero-sum; they coexist, reshaping finance. CBDCs lead in adoption and regulation, cryptos in innovation. Investors should balance exposure, eyeing hybrids for alpha in DeFi and payments evolution.

No comments yet. Be the first!